US Consumer Inflation Falls Sharply to 7.1% Over 12 Months

Major takeaways from the US consumer inflation data

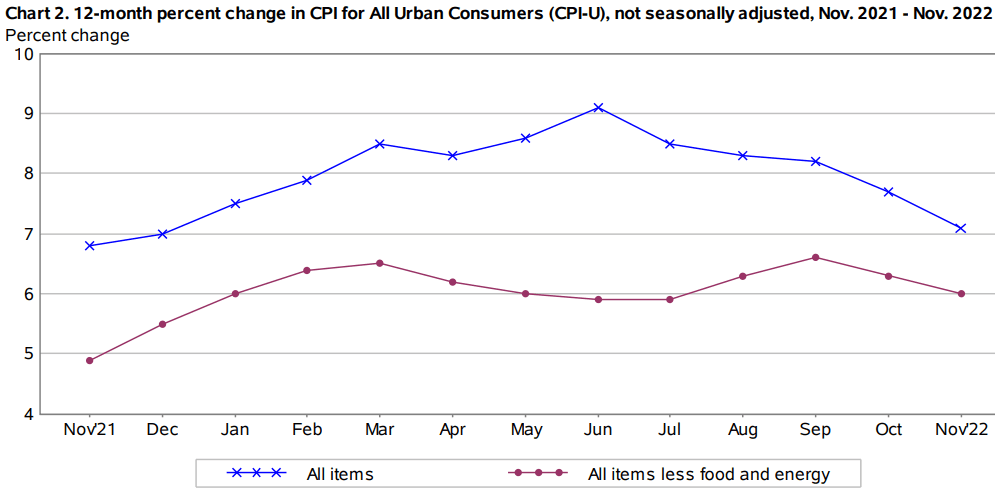

As much as Indian markets are impacted by domestic inflation, even the US inflation sets the tone for Indian markets. That is because the Fed policy still considers the US consumer inflation as a key input for its monetary stance. The good news is that US consumer inflation on a yoy basis has fallen a full 200 bps from its peak of 9.1% in June 2022 to 7.1% in November 2022. The Fed statement will be announced on Wednesday 14th December and there are already talks of a cut in the rate hike by the Fed from 75 bps to 50 bps. This lower inflation should only buttress that argument. Fed rates are already up 375 basis points since the start of March. Here is a sneak peek at the US consumer inflation over last 1 year.

Chart Source: US Bureau of Labour Statistics

The tapering of inflation in the US has been quite rapid since June 2022. US consumer inflation had peaked at 9.1% in June 2022 and has since fallen sharply in the following steps; 8.5%, 8.4%, 8.2%, 7.7% and now 7.1%. what has led this fall in consumer inflation? There has been a visible fall in food inflation and energy inflation, even as lower core inflation stays relatively sticky around the 6% mark. In the latest November 2022 month, food inflation fell from 10.9% in October 2022 to 10.6% in November 2022. In the same period, energy inflation fell from 17.6% to 13.1% while core inflation tapered from 6.3% to 6.0%.

Table of Contents

Here is what we gather from the US consumer inflation trends.

- While headline consumer inflation in the US has fallen 200 basis points since June 2022, it must remembered that we are yet to see the cumulative lag effect of hiking rates. Despite the sharp fall in inflation, food inflation and core inflation is still much higher than historical standards.

- There is a downside risk to any sharp fall in inflation and that is; the weak demand could be an indicator of recession or slowdown fears. Apart from the slowdown risk, the other risk is that if oil continues to remain in short supply due to the Ukrainian crisis, then oil prices could spike in the months to come.

The table below captures the gist of long term inflation and high frequency inflation in the last 2 months.

Category

Nov-22 (YOY)

Oct-22 (YOY)

Nov-22 (MOM)

Oct-22 (MOM)

Data Source: US Bureau of Labour Statistics

There are a few clear trends emerging from the data. Firstly, food inflation has fallen on a yoy basis, but remains 0.5% higher on a sequential basis. In terms of specifics in the food basket vegetables and fresh fruits saw lower inflation while high protein items like meat and dairy products saw a spike in inflation. Food basket is still subject to supply side constraints. Secondly, under the energy category, the fall in energy inflation has been driven by the sharp fall in gasoline prices and natural gas.

Is the Fed going to call a halt on rate hikes?

Not exactly, for starters, the Fed has already reconciled to a 50 bps rate hike in December instead of a 75 bps hike in rates. After 4 hikes of 75 bps each, the overall headline inflation is lower by 200 bps and it may be a very positive indicator. So the rate hikes may not be well and truly over, but it surely look to taper and gravitate towards a more acceptable repo rate. It looks like the rates could settle around the 5.5% or 5.75 % mark.

For the US and India, the relentless and obsessive ursuit of inflation control is over. The focus will have to shift to inflation control and growth boost. This change of heart at the Fed is likely to be beneficial for India too. Now, even RBI can start thinking of easing pressure